FCC makes an extraordinary write-down of 769 million before the capital increase

- The accounting adjustment leads to losses of 788 million at the end of the third quarter

- EBITDA increased by 20% to 587 million and margin increased 13%

- International activity generated 43% of income

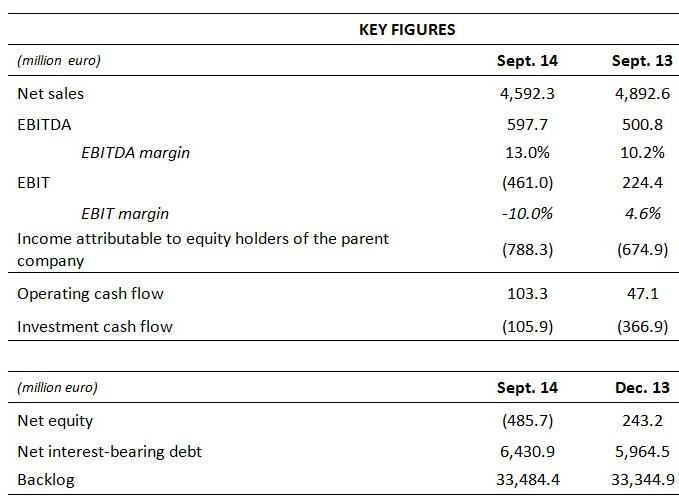

FCC recorded losses of 788 million euros at the end of the third quarter. This result is due to non-recurring provisions and impairments, with no impact on cash flow for the period, for an amount of 769 million to complete the write-down of assets. The accounting adjustment was made just before the General Shareholders’ Meeting announced the proposal for a capital increase of 1 billion euros, the objective of which is to strengthen capital and reserves, reduce debt and improve the income statement.

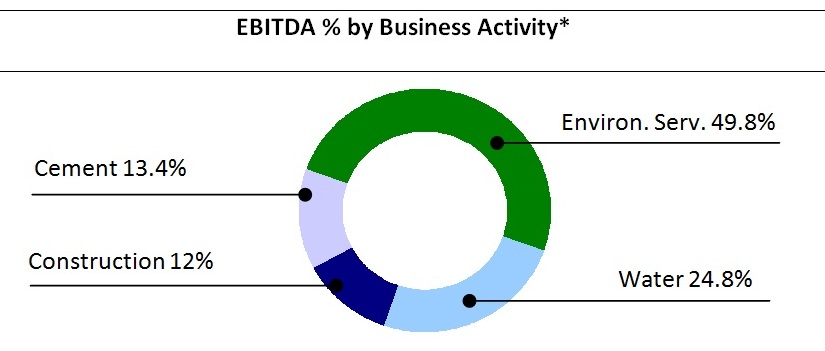

Aside from the impact of the write-downs applied in the third quarter, FCC continues increasing the profitability of its operations, as committed to in the Strategic Plan implemented in March 2013. Along this line, the gross operating result (EBITDA) increased by almost 20% with respect to the same period in the previous year. The 587 million euros obtained is an improvement of 2.8 percentage points on operating margin, which is now at 13%. The increase in profitability is directly related to the savings achieved from the efficiency programme and restructuring measures, especially notable in the areas of Construction and Cement in the Central Services. The areas of Environment and Water contributed 74.6% of EBITDA.

The improvement to the gross result came about with a 6.1% reduction of turnover. Consolidated income was 4.592 billion euros, of which 43% corresponds to international business. United Kingdom and Latin America, with 14.4% and 10.2% respectively, are at the forefront of the Group's international activity, although the region with the highest growth is the Middle East and North Africa due to the Riyadh Metro works (Saudi Arabia).

The net operating result (EBIT) resulted in a negative balance of 461 million euros, due to covering the impact of the provisions for amount of 114 million euros, linked to the value adjustment of real estate assets and various risks in the head of the Group, and the impairment of 655 million on the material assets of FCC Environment, the Environment subsidiary in the United Kingdom. The latter is derived from the plan to close certain landfills that were no longer profitable. Thus, FCC Environment accelerates its transformation process towards the management of urban wastes (recovery, recycling and treatment).

Financial expenses were €363 million, which is 11.8% more than in the same period in the previous year. The financial result covers the new conditions of corporate bank debt in force since 26 June, and includes 40 million in capitalised interest corresponding to Tranche B of the refinancing agreement. Given the destination of the funds captured with the expansion of the capital, the reduction of Tranche B and the financing conditions will result in a substantial reduction of financial costs and, in consequence, will have a positive impact on the consolidated income statement.

The result before taxes, 859 million euros negative, resulted in fiscal credits of 132 million. Adding the losses of 69.9 million calculated on the uninterrupted activities, resulting from the accounting value adjustment of financial derivatives in the area of Energy, from the finalisation of its sale, the net profit attributed to the acquiring company was -788 million euros.

Divestments and portfolio

Net financial debt at the end of the third quarter was 6.430 billion euros. A figure of 40% of this corresponds to the areas of Environment and Water and, inconsequence, is linked to public, regulated and long-term contracts.

If approved by the General Shareholders’ Meeting, the funds collected with the capital increase will directly impact debt reduction and, at the same time, considerably reduce the financial load borne by the Group. It will also enable the net equity situation to be corrected, affected by the losses of recent periods.

Given the implementation of the Strategic Plan in April 2013, divestments of non-strategic assets for a total value of 1.740 billion euros has been made, which is 79% of the objective of 2.2 billion. Added to those made in the last period is the sale of Logistics for 32 million euros, the agreement for the sale of Cemusa (urban furniture) for 80 million euros, and the disposal of FCC Environment (industrial wastes in the United States), in October, for 70 million euros. The assets pending sale include 50% of shares and 36.9% in Globalvía and Realia, respectively.

Finally, the portfolio grew by 0.4%. Of the 33.48 4 billion euros contract, which is equivalent to 5 1/2 years of income, 15.172 billion corresponds to Water; 11.799 to Environment and 6.513 to Construction.

Key Figures September 2014

EBITDA % by Business Activity September 2014